The Generational Oil Roll Happened on Hyperliquid: Why It Couldn't Have Happened Anywhere Else

For the last two weeks, the loudest trade on crypto Twitter has been a short on oil. The big static discount on xyz:CL is mostly gone. The wallet that built the trade has exited. The copycat crowd that piled in behind is still there.

Not ETH, not a memecoin, not a funding-rate scalp. A short on the WTI perp on Hyperliquid, which a month ago barely existed. xyz:CL went from a sleepy HIP-3 market to the single largest book on the venue, bigger than any equity or crypto pair. Traders on X have been trading it, narrating it, and liquidating each other in it on what turned into a generational oil roll.

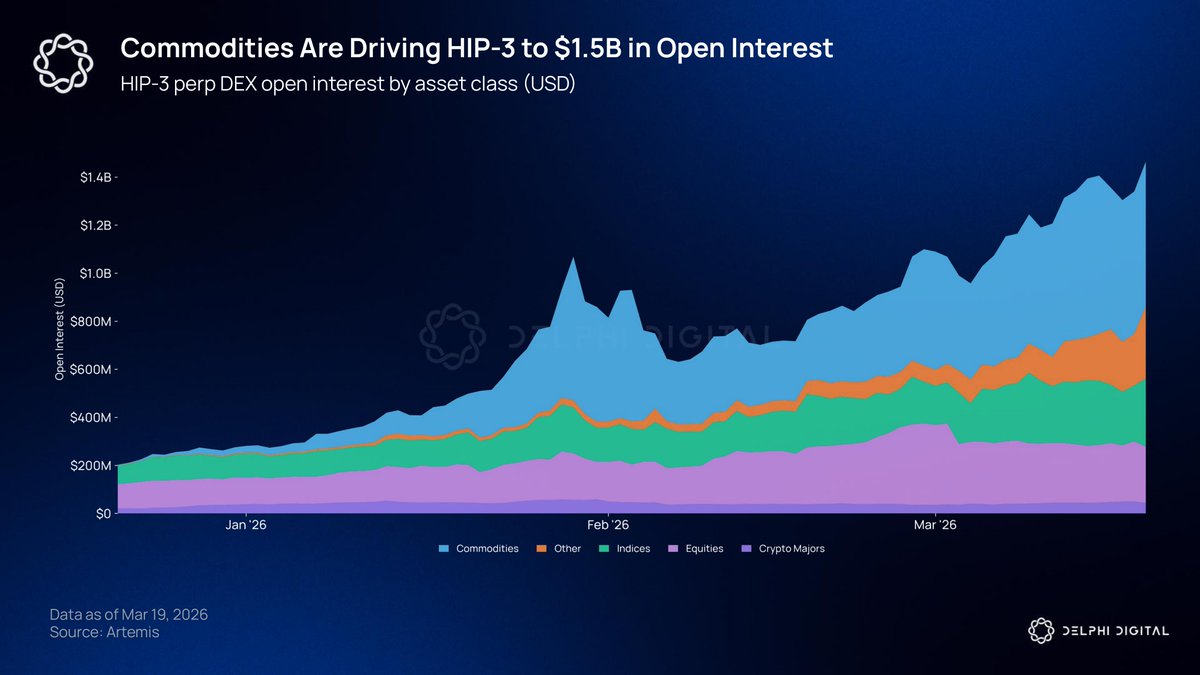

Crude oil is now the single largest market on Hyperliquid's HIP-3. CL currently holds around $300M in open interest, making it bigger than any equity, index, or crypto pair on the platform. Add Brent Oil and you get $482M in combined oil OI alone. Hyperliquid is quickly Show more

What broke about the usual read

If you have traded crypto for any length of time, you have a trained reaction to a -400% annualized funding rate: the shorts are overcrowded, the squeeze is coming, fade the trade by going long and collect the carry. That instinct came from a market where negative funding meant sentiment. Enough traders leaning on the wrong side to pull the mark below the reference, held there by stubbornness, collapsing the moment the move starts.

On xyz:CL the instinct broke.

The shorts were not overcrowded for a sentiment reason. They were overcrowded because the oracle they were shorting was on a published downward walk. Every long who tried to fade the funding got run over by the oracle itself moving lower. The "negative funding means squeeze" heuristic cost people money, because this negative funding was not speculative. It was scheduled.

Good thread, the Hyperliquid Oil markets are the most interesting market in the world right now. If you're not paying attention you're missing out.

x.com/i/article/2041…

The object itself is new. Perps on a dated futures curve, with a scheduled oracle walk between contract months, is not a shape that existed before HIP-3 made builder-deployed perps possible, and it is not a shape any other venue has at meaningful size. The trading community's intuition for what negative funding means was calibrated on BTC and ETH perps whose oracles are simple spot indices. The xyz:CL oracle is anything but simple. If you did not know that, you lost money on the side of the trade that looked obvious.

How the oracle actually walked

xyz:CL is a perpetual, so it does not expire. Instead, its reference walks from the expiring May WTI contract into the cheaper June WTI contract on a published schedule: five 20% steps, one per trading day, spanning April 7 through April 14. When the curve is backwardated, each step drags the reference lower even if crude itself does nothing. In listed futures the trader performs the roll. Here, the oracle does, and the carry shows up as a persistent mark-to-oracle discount and a one-way funding bill from shorts to longs.

The chart above shows all five scheduled steps. Three had landed by April 10 close, with cut 4 due Monday and the finish on Tuesday.

Cut 1: the oil crash bled in

The first scheduled step landed on April 8, and the timing was the story. Overnight, the U.S. and Iran broadcast a de-escalation, front-month WTI crashed ~$115 to ~$93 in a day, and the whole curve re-priced violently.

TWO-WEEK CEASEFIRE DEAL Trump says he will pause planned attacks on Iran for two weeks after talks with Pakistan’s leadership and on the condition that Iran immediately and safely opens the Strait of Hormuz. He claims U.S. military goals have already been achieved and that Show more

On a normal day, a scheduled 20% step down from pure May into an 80/20 May-June blend is a smooth push lower. On this day, it happened inside a 16% price collapse. The oracle dropped for two reasons at once: the underlying dropped, and the scheduled weighting had shifted. WTI funding bottomed at -625% annualized in the 24-hour window around the cut. Shorts were still directionally right but getting buried by the funding bill. Longs who tried to fade the funding got run over by the price move on top of the scheduled step. There was no safe side of the trade for a full day.

By the close of April 8, the perp sat around $91 against an oracle around $92, roughly 100 bps under. Inside fair band, but not comfortably.

Cut 2: the bottom

Cut 2 landed on April 9, shifting the oracle from 80/20 to 60/40 May-June. The oil crash had widened the May-June calendar spread to $8.32, so a 20% step through that curve was a bigger dollar move than cut 1 had been. WTI funding hit -729% annualized at the cut hour itself and reached -855% in the hour after, the worst per-cut funding print of the roll.

Then the gap started closing. On Apr 8 close, the perp had been ~100 bps under oracle. Twenty-four hours later, with one more cut consumed and the remaining walk visibly shorter, the mark converged. By late New York on April 9, the perp was 35.6 bps below oracle, comfortably inside the public no-arbitrage fair band. The big gap that had defined the trade was mostly gone.

Fair value, after the cut

The math behind the hero above: a 60/40 blend of the last completed Databento minute, $98.71 May and $90.39 June, gives $95.382, a rounding error from the live oracle at $95.387. The perp was $95.047. The useful comparison is the live spread against the public no-arbitrage band:

The market implies 12.1 hours of effective smoothing, inside the 8 to 16 hour window. The public model and the live market are, for the first time in two weeks, saying roughly the same thing.

But a fair-value print is a point-in-time read. The positioning underneath it is something else.

The biggest wallet in the book

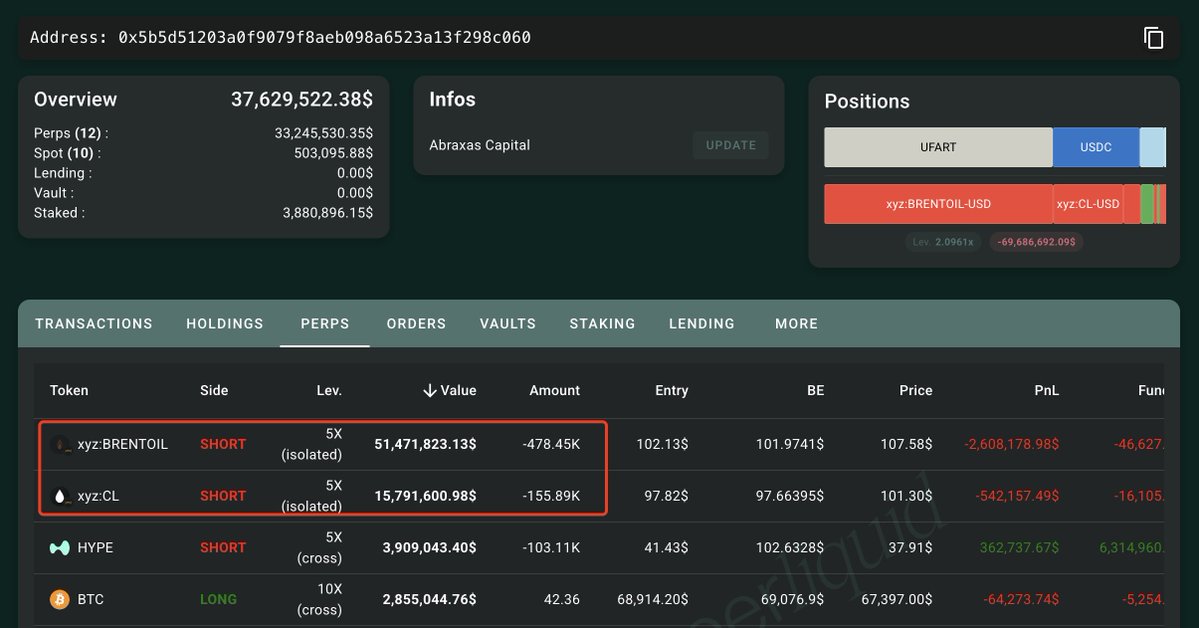

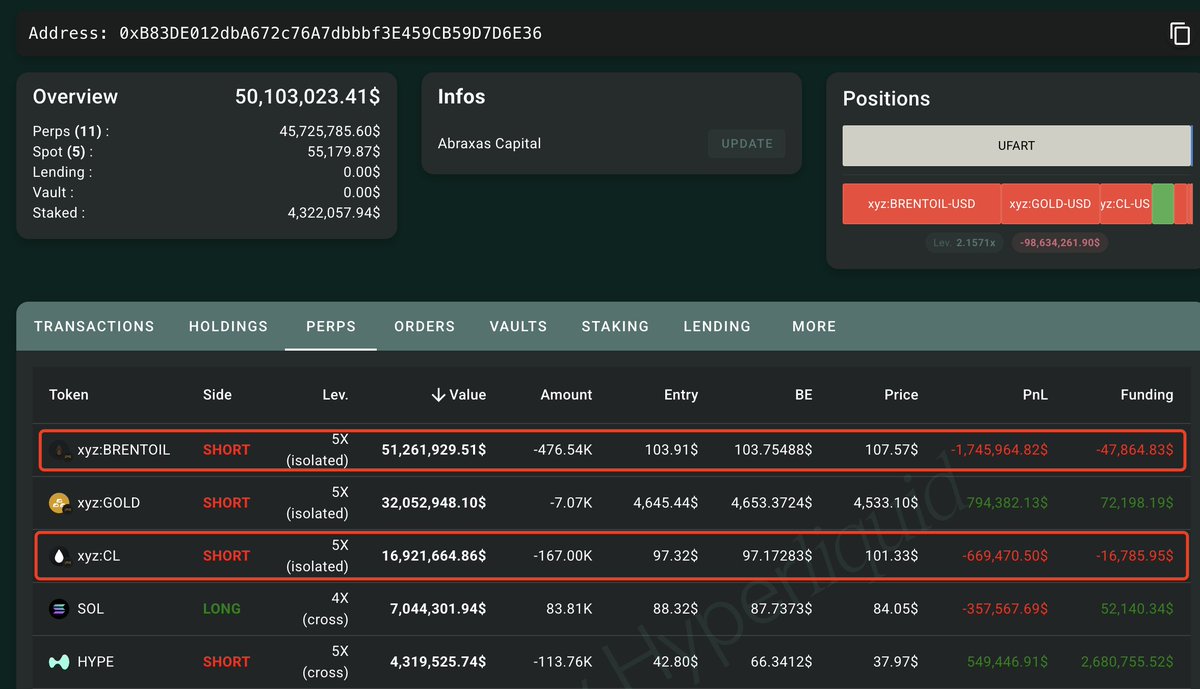

Every crowded trade has a largest participant. For the oil roll, that was Abraxas Capital, a London-based macro manager that was visibly short both xyz:CL and xyz:BRENTOIL for most of early April across two wallets. What they were actually doing underneath the visible leg is harder to answer from on-chain data alone.

On March 30, lookonchain put the position on Twitter:

Abraxas Capital has built a massive $135M short position on crude #oil futures, including: • 954,996 xyz:BRENTOIL ($102.7M) • 322,885 xyz:CL ($32.7M) hypurrscan.io/address/0xB83D… hypurrscan.io/address/0x5b5d…

The trade did not start there. The basis was visible to anyone who read the trade.xyz roll schedule, and other wallets had been running pieces of it for weeks. The lookonchain post just surfaced the largest single participant. After it dropped, every wallet that saw the position and decided to copy it piled in, without necessarily running the same hedge, conviction, or sizing. That is the cohort that is still in the book.

Abraxas's own book peaked above $165M combined notional through early April. Their Hyperliquid-side funding bill was reportedly north of $1.7M on a single position, roughly $120k per hour during the most active windows. When the Iran ceasefire crashed front-month WTI 16% on April 7, Abraxas started trimming the Brent leg. They held $127M through the worst of cut 2's funding pain on April 9, and fully closed xyz:CL and xyz:BRENTOIL between April 9 and April 10. By the April 10 holder snapshot[source], both wallets hold zero oil.

Whether the trade paid at all depends on legs we cannot see. If they were running an oracle-roll basis arb (short the front-month-referenced perp against a long June WTI contract on CME, collecting the convergence as the oracle walks from pure May into pure June), the Hyperliquid funding bill is an expense on one side of a hedge and the PnL lives in the other leg. If they were running a directional short unhedged, the April 7-8 ceasefire crash handed them the directional payoff on top of whatever oracle drift they captured. Community reads have gone both ways on this, and public attribution only shows the Hyperliquid side. We are not going to pretend to resolve it. What is visible is that the largest wallet in the book is no longer in the book.

The crowd that followed them in is.

The structure did not move

Two questions decide whether the remaining crowd actually cleared: did the carry migrate to other venues, and did the shorts thin out. Both answers are no.

First, the carry did not migrate.

trade.xyz cleared 99.08% of oil volume and held 98.58% of open interest. WTI paid $4.9k per day per $1M to longs, oil turned over 2.59x/day, and funding was negative for 24/24 hours. The smaller venues looked like contrast cases, not real carry books.

Second, the shorts did not thin out.

The April 10 holder map shows 923 WTI shorts and 438 Brent shorts, with the top 10 holding 67% of WTI short notional and 86% of Brent. Brent is the thinner, more fragile book. WTI is the larger, more liquid confirmation book. If an unwind starts, Brent should move first. WTI tells you whether that first crack becomes a squeeze or just another roll step getting repriced.

The single largest short still in the book holds roughly $74.7M across WTI and Brent combined, at 20x leverage, out of a $39.7M account. The wallet is 0x9d32...aff5, publicly attributed on X to Hyperithm. That is not Abraxas Capital. The top two shared-cohort wallets alone carry more combined short exposure than Abraxas held at its peak.

Cut 3 and the weekend freeze

Cut 3 landed on April 10 at 20:00 UTC, walking the oracle from 60/40 to 40/60 May-June. WTI funding hit -566% at the cut hour and -727% in the hour after, milder than cut 2 in both prints and the third-deepest cut of the roll. The mechanic was behaving. Then CME closed for the weekend, and the trade stopped looking like a roll story.

CME closes Friday night. The oracle is a blend of CME contracts, so the oracle freezes too. Hyperliquid is 24/7. For two days, every dollar of flow on the perp moves the mark against a reference that cannot fight back. The Saturday chart is what that looks like in real time.

This is the cohort that ran cut 3. On April 10, the top ten wallets in the shared short book traded $324M on Hydromancer's fills tape and opened 2.14M new contracts of short. Long-side flow from those ten wallets was zero. They were not covering. They were trimming the older in-the-money shorts and immediately re-shorting at the new oracle level. The two heaviest one-sided sellers that day, 0x3037...1e83 and 0x17c3...a868, are unattributed wallets sitting on $30M+ combined shorts against accounts a quarter their size.

So when the Saturday print hit, it did not hit a balanced book. It hit a book where the dominant participants had just stacked fresh shorts at $95 the day before, and where the heaviest weight is sized so the drawdown is not theirs to absorb in isolation. A properly-hedged oracle-roll basis arb cannot rebalance until CME reopens Sunday night. Every weekend funding print is unhedged carry. Cut 4 lands Monday at 20:00 UTC, a few hours after that reopen. The book that eats the Saturday swing is the same book that has to absorb the next scheduled step.

What to watch for

Static gap priced, crowd still in place: the next move is conditional. A fresh widening without a wider May-June curve is interesting. A squeeze higher while shorts are paying is interesting, especially if Brent moves harder than WTI. A quiet grind where the spread stays inside band and funding slowly normalizes is not.

What would make this read wrong

The mistake from here is overclaiming a static edge that is no longer there. A balanced market can widen again without the perp being freshly wrong. The path can stay expensive to own even if the spread looks fine.

Why we think Hypercall matters for this

Everything above is what traders had available to figure the trade out in real time: a live Hyperliquid feed, a CME futures curve, a holder snapshot, some community attribution on X. Each piece is its own data source. Stitching them into a view of the perp was manual, slow, and not something you could repeat across every HIP-3 market on the way.

A rolling commodity perp has three distinct inputs that don't travel together in listed markets: a crude direction, the dated calendar spread that sets the remaining oracle cuts, and the crowd leaning on one side of the book. Listed futures options price a single month at a time and have no natural home for any of those pieces together. "Oil vol" on CME is the vol of one dated contract. The thing that actually drove the trade.xyz roll was the expected walk across a curve blend, and the expected behavior of the cohort holding the short through it. A month-at-a-time option never touches that.

Hypercall is built around the other decomposition:

- Scheduled carry belongs in fair value. The remaining oracle cuts are published. They are not volatility. A vol surface that charges premium for them is wrong.

- Curve uncertainty belongs in ATM vol. If the May–June spread re-prices, the perp's reference re-prices with it. That is the part a real vol model should own.

- Crowded positioning belongs in skew and jump risk. A squeeze is not normally distributed. If 85 shared-cohort wallets unwind into the final cut, the move is discontinuous. That is upside skew and short-dated convexity, not realized vol.

A venue that separates those three inputs can quote an option on the rolling perp that the instrument actually deserves: scheduled carry priced into forwards, curve risk priced into ATM, crowd risk priced into skew. None of that is hypothetical, the trade.xyz roll this April made the case for it in real time. That's the problem we're building around.

The takeaway

The loudest trade of the last two weeks stopped being a fair-value trade somewhere around Apr 9. It turned into a positioning trade. The wallet that built it is gone. The crowd that followed it is still inside, still exposed to one more scheduled cut on Monday and a final print on Tuesday, and currently sitting on a frozen-CME weekend with funding swinging by hundreds of percent annualized in a single hour.

Three things fall out of that:

- The static edge is priced. If your thesis was "the perp is wildly cheap," it is no longer the right claim to defend. The model caught up.

- The path is still the interesting object. Who breaks first, Brent or WTI. Whether the crowd clears on cut 4 or rolls all the way to the finish. Whether funding normalizes or spikes again.

- This is what a rolling perp with a dated oracle actually looks like, and it is not what listed futures options price cleanly. Scheduled carry is not volatility. Curve uncertainty is not the crowd. A venue that can separate the three is the one that can actually quote this instrument.

That last one is why we write these at all.