Options vs Perpetuals

Options and perpetuals both give you leveraged exposure to an underlying asset. But they do it in fundamentally different ways, with different risk profiles, different costs, and opposite relationships to volatility.

This page breaks down the differences visually so you can build intuition for when each instrument makes sense.

The Path Problem

The single most important difference: options are path-independent, perps are path-dependent.

An option buyer's PnL at expiry depends only on where the underlying price ends up. It does not matter if the price crashed 50% in the middle, as long as it recovers by expiration.

A perp holder does not get that luxury. Because perps have a liquidation price, a temporary drawdown can turn into a permanent loss. The path the price takes matters as much as the destination.

Options care about where you end up. Perps care about every step of the journey.

Why the path matters

With a perp, you post margin (collateral) to open a leveraged position. If the position's unrealized loss exceeds your margin, you are liquidated: the position is force-closed, and your margin is gone. Even if the price immediately recovers, your position no longer exists.

With an option, your maximum loss is the premium you paid. There is no margin call, no liquidation trigger, no forced exit. The price can swing wildly during the life of the option and it changes nothing about your payoff at expiry.

Long Volatility vs Short Volatility

This path dependence creates a fundamental difference in how each instrument relates to volatility.

Options: Long Volatility

Big moves help you

- Convex payoff: gains accelerate, losses are capped

- Higher volatility = higher option value

- Drawdowns during the trade do not affect final PnL

- You pay a fixed cost (premium) for this protection

- Time works against you (theta decay)

Perps: Short Volatility

Big moves hurt you

- Linear payoff with a cliff: gains and losses scale equally until liquidation

- Higher volatility = higher chance of hitting the liquidation wall

- A single bad drawdown can permanently end the trade

- You pay an ongoing cost (funding rate)

- Time is neutral (no expiry), but funding accumulates

The payoff shapes tell the story

The option payoff curve bends in your favor: gains get bigger faster than losses. This is convexity.

The perp payoff is a straight line that terminates at liquidation. No curve, no bend, no protection.

Convexity is the difference

An options buyer benefits from big moves. A perp holder fears big moves. Same underlying asset, opposite volatility exposure. The option's curve is what you're paying premium for.

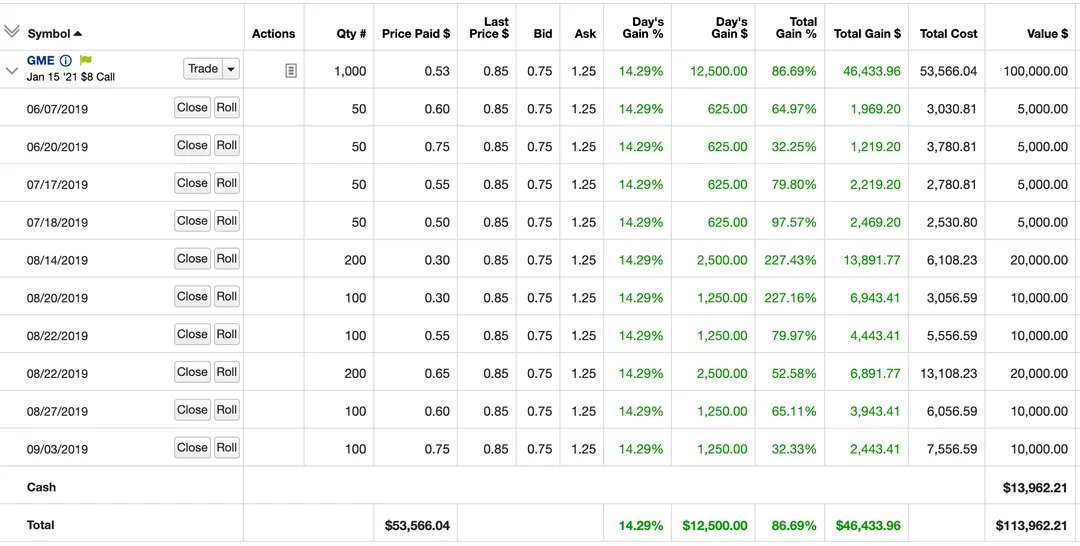

Case Study: The Roaring Kitty GME Trade

Roaringkitty made like mid 9 figs no? Is there a single meme coin outside of trump that someone cashed that lol

Imo - @TheRoaringKitty is a great example here on where options shine vs perps. If you were to model Roaring Kittys GME trade on equity perps (assuming no funding, no fees, etc) he'd have gotten liquidated within 40 days. Embedded leverage was ~7-13x (S/prem on $8 calls) If he Show more

This is path dependence in action. DFV (Roaring Kitty) held deep out-of-the-money call options on GameStop with significant embedded leverage (~10x). The stock price was wildly volatile before the final squeeze, with drawdowns that would have wiped out a leveraged perp position multiple times over.

But the options did not care about the path. They only cared about where GME was at expiration.

The chart below uses actual GME weekly closing prices from June 2019 through February 2021. Adjust leverage and funding rate to see approximately when a perp position gets liquidated — and what DFV's options returned instead.

Greeks are Just Precise Funding

If you already understand how perp funding works, you have intuition for what the Greeks measure. The Greeks are not a separate concept; they are a more precise vocabulary for dynamics that perp traders already navigate.

| Greek | What it measures | Perp equivalent |

|---|---|---|

| Theta | Daily cost of holding the option | Funding rate: periodic cost of holding the perp |

| Delta | Price sensitivity to underlying | Position size: 1 perp = delta of 1 |

| Gamma | How delta changes with price | No equivalent (this is the edge) |

| Vega | Sensitivity to volatility changes | Sensitivity to funding rate shifts |

The key difference: Gamma

Funding on a perp is like paying theta on an option. Both are ongoing costs of maintaining a directional position.

But with options, you get something valuable in return for paying theta: gamma. Gamma means your effective position size grows as the trade moves in your favor, and shrinks as it moves against you. This is the convexity in the payoff curve. Your winners automatically compound, your losers automatically fade.

With perps, you pay funding but your position size stays fixed. No convexity. No gamma. Just a straight line with a cliff at the end.

Theta is the rent. Gamma is what you're renting. Perp funding is rent for a straight line. Option premium is rent for a curve.

Perps vs Spot

Before comparing options to perps, it helps to understand what a perp actually is: synthetic spot with built-in leverage.

Spot

Own the asset

- Full capital locked ($100k for 1 BTC at $100k)

- No liquidation, no margin calls

- No ongoing costs

- Simplest form of exposure

Perpetual

Synthetic spot + leverage

- Fraction of capital locked ($10k at 10x)

- Liquidation if price moves against you

- Ongoing funding payments

- Capital efficient, but path dependent

Option

Convex exposure

- Premium only ($10 for an ATM call)

- No liquidation, max loss is premium

- Time decay erodes value daily

- Capital efficient with built-in protection

A perp is essentially a margin loan on the underlying. You borrow most of the position value and pay interest on it through the funding rate. The funding mechanism keeps the perp price anchored to spot: when the perp trades at a premium, funding is positive (longs pay shorts), incentivizing arbitrage back to parity.

When to Use Each

| Scenario | Instrument | Why |

|---|---|---|

| High conviction, volatile path expected | Options | Survive drawdowns, benefit from the volatility |

| Low conviction, want to explore | Options | Defined risk, can size up without fear of liquidation |

| High conviction, low vol expected | Perps | Cheaper carry if funding is low and no big drawdowns |

| Short-term scalping | Perps | Linear PnL, no time decay on short holds |

| Hedging existing spot | Perps or Options | Perps for linear hedge, options for tail protection |

| Earnings/event plays | Options | Convexity captures outsized moves |

| Yield/income generation | Short options | Collect premium from theta decay |

Not either/or

Most sophisticated traders use both. Perps for short-term directional trades where the path is predictable. Options for longer-term positions, event trades, or anytime the path is uncertain. The instruments are complementary.

See Also

- Greeks Overview - What the Greeks measure

- Implied Volatility - Why IV drives option prices

- Vol Regimes - When volatility spikes and calms

- Lesson 1: What is an Option? - Start from the basics